The UK left the European Union (EU) on 31 January 2020, entering a transitional period that finalises on 31 December 2020. From 01 January 2021 new VAT rules apply and businesses need to get ready for them.

Domestics VAT rules remain the same for transactions within the UK.

From 01 January 2021, UK businesses will have to treat EU countries like they do countries outside the EU. All VAT transactions with EU countries will be treated as Imports and Exports, as the concept of Dispatches and Acquisitions will no longer apply.

IMPORT VAT

Imports with a value greater than £135

At present, when goods arrive in the UK, VAT is applied. The VAT can be paid at the time of entrance, and HMRC will send to the business a C79 report monthly indicating all the VAT paid during the month. In addition, HMRC have introduced a new system called: “postponed VAT accounting system”. This is similar to the existing Reverse Charge mechanism, whereby import VAT is not physically paid upfront and then reclaimed on the subsequent VAT return. Instead, it is accounted for as input and output VAT on the same VAT Return. Although postponed VAT accounting is optional, it becomes mandatory if the business defers the submission of customs declarations. It is worth remembering that postponed VAT accounting can now be used for all imports outside of the EU too.

Purchases of services from business to business remain subject to tax in the country of the customer. Rules are same than before Brexit.

Imports with a value under £135

- B2C (Business to Consumer) – Suppliers will need to register for VAT in UK and charge UK VAT when the consumer buys from them.

- B2B (Business to Business) – Reverse Charge procedure will apply. Buyers will need to make sure the suppliers know their VAT Number, otherwise they will be charged with VAT as B2C.

EXPORT VAT

Exports to EU countries will be treated as exports to the rest of the world and as Zero rated for UK VAT registered persons, regardless of whether goods are exported to business or consumers.

It is most likely that businesses carrying out B2C transactions in EU will need to register in their customers countries and deal with local VAT requirements.

Under the place of supply rules, B2B sales of services will continue to be generally subject to tax in the country of the customer and administered through the Reverse Charge system, with some exceptions.

B2C sales of services will continue to be generally subject to tax in the country of the seller, again with some exceptions.

TRIANGULATION

Up to 31 December 2020, triangulations between EU countries were simplified, treated as zero rated intracommunity supplies, with the “middleman” not required to register for VAT in the country where the goods were delivered.

From 01 January 2021 the situation will change and the impact of these changes on businesses will depend on their role of in the chain.

1. UK Middleman

Scenario: UK company buys goods in France and sells to Italy. The transport of the goods is from France to Italy.

In this case, where the UK Company is the middleman, the French company will issue a zero-rate invoice and the UK company must register in Italy for VAT and charge Italian VAT to the Italian company. If the UK company cannot provide the French company with an EU VAT number, the French company will have the obligation to charge French VAT on their invoice to the UK company.

2. UK Manufacturer

Scenario: the UK Company sells to France and the goods are delivered to Italy.

In this case the goods are exported from the UK to Italy. For the Italian and French companies there will be some Import charge depending on their internal rules and Intercoms of the operation.

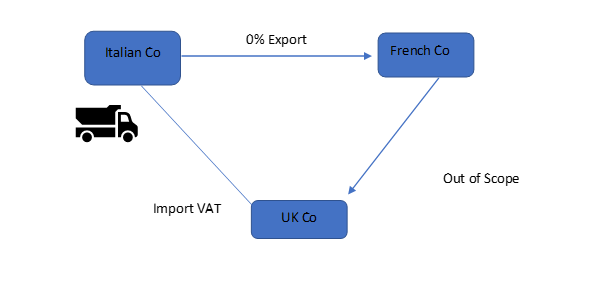

3. UK Final Consumer

Scenario: the UK Company buys the goods from a French Company and receives the goods directly from an Italian Company. The goods will be charged with import fees at their arrival in the UK.

All information is current at the time of publishing.